- Global M&A dollar value of closed deals for Q1 2019 totaled $435B, ↓ 29% compared to 4Q 2018. Deal count dropped 5% for the same time frame. Compared to Q1 2018, Global M&A $ volume was ↑23%, however, deal count was down on a YoY basis.

- U.S. M&A dollar volume was down on QoQ basis however, YoY it increased 31%. M&A deal count was up ↑11% QoQ basis, however, YoY it decreased 45% while dollar volume was down QoQ for Q1 2019 vs. Q4 2018.

- Global Private Placements totaled $58B in Q1 2018, ↓34% from Q4 and ↓48% YoY. Similarly, North American Private Placements for all sectors totaled $44B, ↓31% QoQ and ↓50% YoY while deal count was ↓3% QoQ and ↓38%YoY.

- In N. America, the Digital Health M&A deal count on a QoQ basis was essentially flat with at a nominal 2% increase. Of note, Q1 dollar volume decreased by 86% compared to Q4 2018. However, if the Athenahealth deal is excluded, Q1 $ volume was ↓ 34%. YoY dollar volume was down 85%. The largest announced deal in Q1 2019 was Symplr’s acquisition of API Healthcare for $300M.

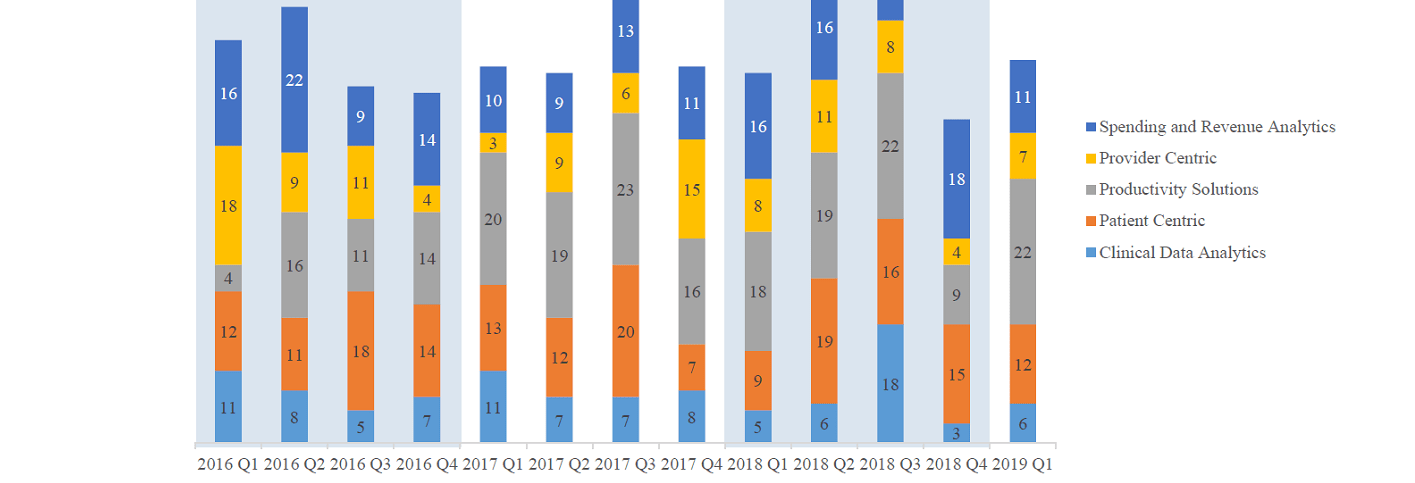

- For Q1 2019, Productivity Solutions was the most active in terms of deal count, accounting for 39% of M&A deals. The Spending & Revenue Analytics as well as the Patient Centric Subsectors each accounted for approximately 20% of M&A deals for Q1 2019.

- For Q1 2019, Productivity Solutions was the most active in terms of deal count, accounting for 39% of M&A deals. The Spending & Revenue Analytics as well as the Patient Centric Subsectors each accounted for approximately 20% of M&A deals for Q1 2019.

- Private placement transactions in the North American Digital Health sector were essentially flat in Q1 2019 both QoQ and YoY, ↑4% and 2%, respectively. Disclosed $$ investments in North American based HIT firms declined 21% YoY and 25% QoQ.

- After the December correction, the stock market has bounced back and continues to strengthen. We expect valuations for private placements to remain high due to a large pool of uninvested VC capital and as long as the stock market remains positive.

- There were no Digital Health IPO’s in Q1 2019 as well as all of 2018. However, both Livongo and Change Healthcare have filed for IPO registration which may be an indication that the capital markets are willing to embrace a high valuation expectation in the case of Livongo, and accommodative to the funding needs of Change Healthcare.

- As of LTM Q1 2019, Novahill’s Digital Health Public Comparable Index outperformed the S&P 500 Index, gaining 15% compared to 8% for the S&P 500. Digital Health companies continue to trade at premiums twice as high as the S&P 500 in regards to EV to both EBITDA and Revenues.

2019-04-26